Inflation prevails. The market (including Goldman Sachs and me) has grossly undervalued the Fed. Maybe one day the market will get it right.

From WOLF STREET by Wolf Richter.

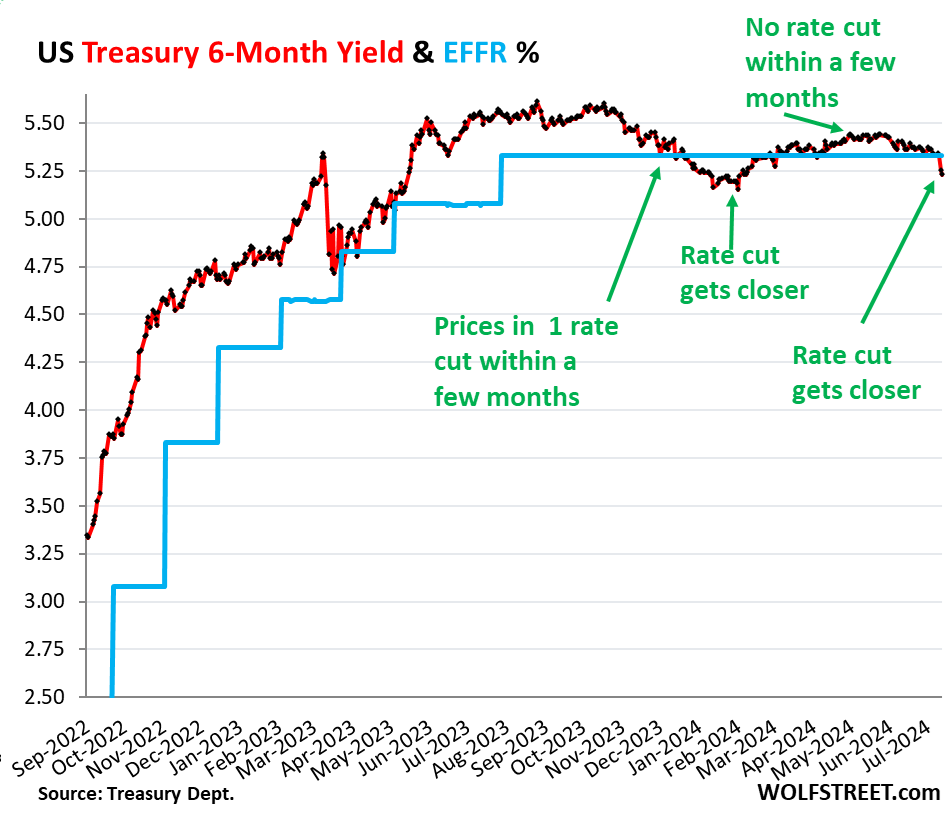

The release of the Consumer Price Index (CPI) report on Thursday, which came in at -0.056% (rounded to -0.1%) month-on-month, caused the 6-month Treasury yield to fall 8 basis points, before dropping another 2 basis points to 5.23% on Friday. This combined 10 basis point drop was the most visible move in two days.

This has pushed the six-month yield just below the lower end of the Fed’s target range for the federal funds rate (5.25% to 5.50%) and below the effective federal funds rate (EFFR), which currently stands at 5.33% (blue in the chart below).

So the six-month yield, having already mispredicted earlier this year, is now pricing in one rate cut within six months, with the emphasis on the first two-thirds or so of that period.

From late November through January, the 6-month yield was pricing in a rate cut within a 6-month time frame. By February 1, the yield had fallen to 5.15%, indicating that the market was confident that a rate cut would occur at the March FOMC meeting.

But the markets were wrong: Inflation rates were low across the board in January, February, March and April, and interest rates still have not been cut.

In March and April, inflation measures worsened and a rate cut in the six-month yield over the six-month horizon was taken off the table.

Inflation readings in May were much weaker, and Thursday’s June CPI report put a rate cut back on the agenda, with an emphasis on the first two-thirds of the term within the six-month yield horizon.

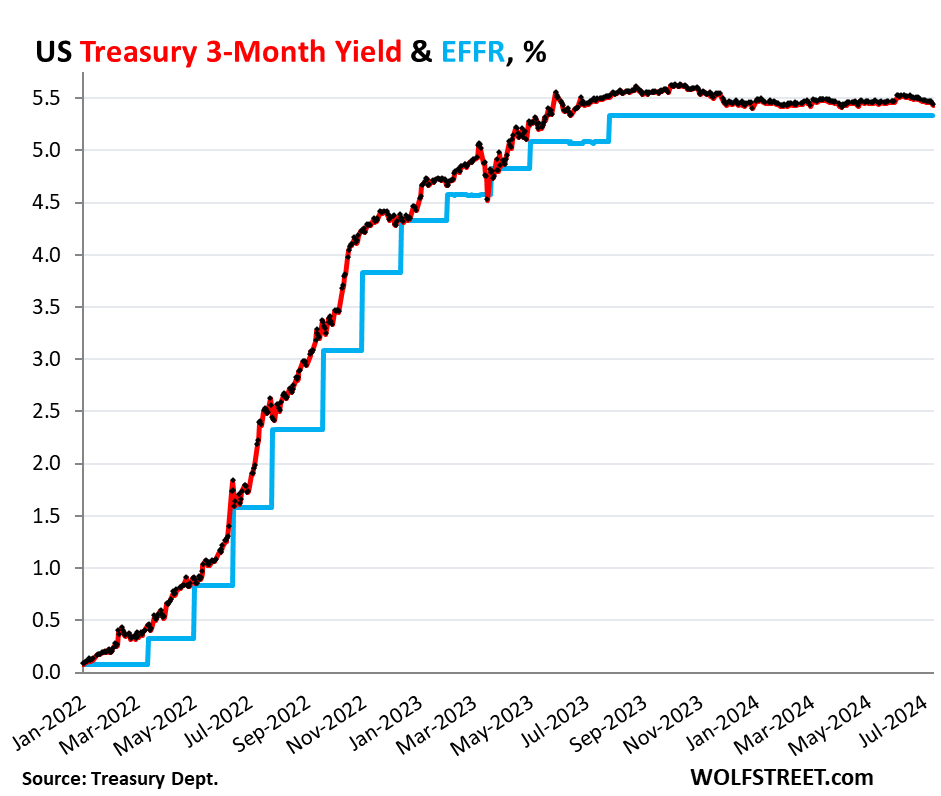

However, short-term bond yields are not pricing in any rate cuts in the near term. Short-term bond yields have not moved much since the CPI report and are both near the upper end of the Fed’s policy rate (5.5%) and above the EFFR (5.33%).

- 1-month yield: +1 basis point to 5.47%

- 2-month yield: +2 basis points to 5.52%

- 3-month yield: -3 basis points to 5.43%

- 4-month yield: -5 basis points to 5.41%

In other words, the Treasury market doesn’t expect a July rate cut at all, but sees a September cut as likely — not as likely as the late January prediction that a rate cut would almost certainly come by March, which never materialized.

The 3-month yield is not seeing a rate cut within the first two-thirds of the time horizon. There was no rate cut in July, and the September 18th FOMC meeting statement is over the first two-thirds of the time horizon, so the impact on the current 3-month yield is small.

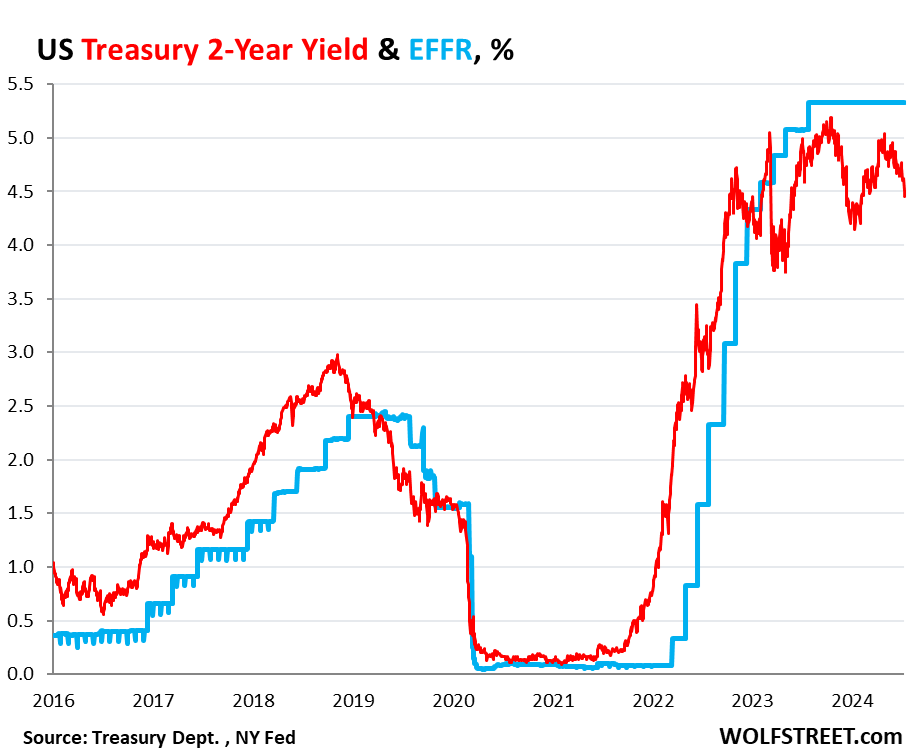

The market has been wrong on 2-year Treasury yields all this time.

The 2-year Treasury yield shows that the bond market has been wrong about the Fed’s rate hikes and cuts all this time: It expected much fewer and smaller hikes than the Fed ultimately took, and it started pricing in cuts before the Fed even stopped hiking, without ever rising to a level that would price in the actual interest rate that the Fed has held for nearly a year.

So back in April 2022, the 2-year Treasury yield was around 2.5%. 2.5% sounds like a terrible yield now, but at the time, after 15 years of near 0% followed by several years of rising yields, which had risen to around 2.4% in 2019, 2.5% sounded pretty good and the market thought that was pretty close to the Fed’s final interest rate.

In February 2022, before the Fed began hiking rates, Goldman Sachs projected that the Fed would raise interest rates seven times in 2022, each by 25 basis points, followed by three 25-basis-point hikes, one per quarter, in 2023, reaching a final target range for the federal funds rate of 2.5% to 2.75% by the third quarter of 2023.

In all, the Fed took more than double that amount of action by July 2023.

So, the two-year bonds sold at auction in April 2022 seemed like a good deal, with a coupon of 2.5% and a yield close to that, so we, as part of the government bond market, bought a few. Two years was the limit. The rest of the bonds were short-term bonds.

These 2-year notes matured in April 2024, paid their face value, and earned about 2.5% interest per year for those two years. The entire market was wrong, and so were we. The Fed was scheduled to raise rates to 5.25-5.5% by July 2023, more than double the yield we received, and those rates are still there, with 2-, 3-, and 4-month T-bills yielding well above the 2-year notes.

The two-year note yield closed at 4.45% on Friday. The market has never expected the Fed to keep interest rates above 5% for an extended period of time, but the Fed has kept them above 5% for over 14 months. Also, the two-year note yield has been below the EFFR for almost every month since January 2023, turning Thomas skeptical.

The market was wrong about Fed interest rates, and all of the 2-year notes maturing in or due to mature in 2024 purchased at auction were terrible trades. Buyers would have been better off buying a series of short-term T-bills that are more closely tied to the Fed’s actual policy rate, rather than following market expectations.

At some point, the market will get its rate cut prediction right. But it will take just a few more inflation readings to postpone the cut further. Friday’s producer price index showed a spike in services inflation, marking a clear U-turn in December. Producers who pay higher prices for services will try to pass it on, which could eventually be reflected in consumer prices and drive inflation readings higher in the coming months. Alternatively, if producers are unable to pass on the higher service prices, profit margins will be squeezed.

Inflation is unpredictable. History shows that once inflation emerges on a large scale, it tends to come in waves and produce surprises, which it has done many times before, including in the first four months of this year.

Enjoy reading WOLF STREET and want to support us? You can donate, we’d be so grateful! Click on Beer and Iced Tea Mugs to find out how.

Want to be notified by email when WOLF STREET publishes a new article? Sign up here.

![]()