analysts are quite bullish on the company’s stock following its recent performance.")

Micron Technology, Inc. (NASDAQ:MU) shareholders are probably a bit disappointed, as the share price fell 5.7% to US$132 in the week following the latest Q3 earnings release. Operating results were on track, with revenues of US$6.8b, 2.0% above expectations, and statutory earnings per share of US$0.30, in line with analysts’ estimates. The analysts typically update their forecasts at each earnings release, and from their estimates we can gauge whether their view on the company has changed or if there are any new concerns to look out for. With this in mind, we’ve gathered the latest statutory forecasts to find out what the analysts are expecting for next year.

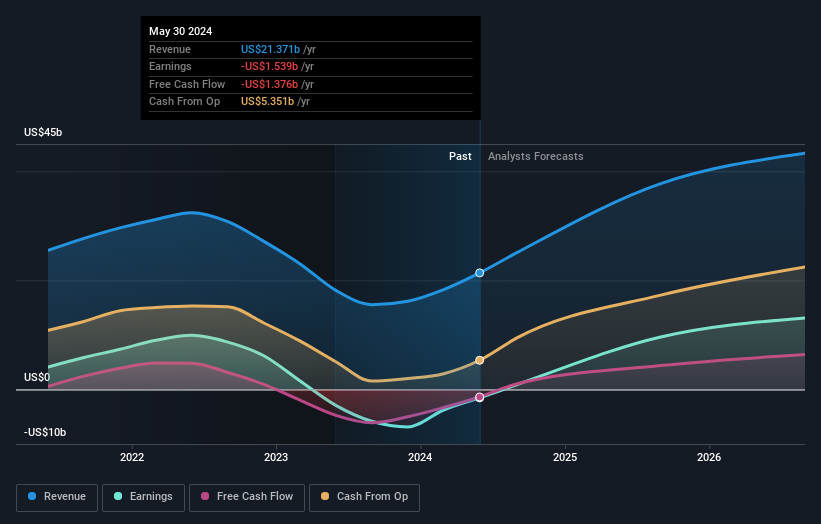

Read our latest analysis for Micron Technology

Taking into account the latest financial results, the latest consensus for Micron Technology from 37 analysts is for revenues of US$37.7b in 2025. If achieved, this would represent an impressive 77% increase on revenues over the past 12 months. Revenues are expected to improve, with Micron Technology expected to report statutory profits of US$8.71 per share. Prior to this earnings report, analysts had been forecasting revenues of US$36.7b and earnings per share (EPS) of US$8.47 in 2025. Sentiment appears to have improved slightly following the latest results, with analysts now being slightly more optimistic in their forecasts for both revenues and profits.

With these upgrades, it’s not surprising to see analysts raise their price target by 7.3% to $158 per share. However, it’s unwise to fixate on a single price target, as the consensus target is effectively the average of analysts’ price targets. As a result, some investors prefer to look at the range of estimates to see if there are any divergences in opinion on the company’s valuation. There are mixed perceptions on Micron Technology, with the most bullish analyst valuing it at $225 per share and the most bearish at $90.00 per share. This is a fairly wide spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

While these estimates are interesting, it’s useful to paint a broader picture when comparing forecasts to Micron Technology’s past performance and industry peers. For example, Micron Technology’s growth rate is expected to accelerate significantly, with annualized revenue predicted to grow at 58% by the end of 2025. This is a significant increase over the 2.4% annual decline over the past five years. In contrast, our data suggests that other companies in the industry (those with analyst coverage) are expected to grow their revenue at 18% per year. Not only are Micron Technology’s revenues expected to improve, but it appears that analysts are predicting faster growth than the industry as a whole.

Conclusion

Most importantly, the analysts have increased their earnings per share forecasts, suggesting a clear increase in optimism for Micron Technology following these results. Encouragingly, the analysts have also increased their revenue forecasts, which now expect the business to grow at a faster pace than the broader industry. Price targets have also increased, as the analysts clearly feel that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company’s earnings is much more important than next year. We have forecasts for Micron Technology out to 2026, and you can see them free of charge on our platform.

But before you get too excited, we discovered 1 warning sign for Micron Technology Something you should know.

Valuation is complicated, but we can help make it simple.

investigate Micron Technology By checking our comprehensive analysis, you can see whether it may be overvalued or undervalued. Fair value estimates, risks and warnings, dividends, insider trading, financial strength.

View free analysis

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

Valuation is complicated, but we can help make it simple.

investigate Micron Technology By checking our comprehensive analysis, you can see whether it may be overvalued or undervalued. Fair value estimates, risks and warnings, dividends, insider trading, financial strength.

View free analysis

Have feedback about this article? Concerns about the content? Contact us directly. Or email us at editorial-team@simplywallst.com