mixed financials the reason for its lackluster performance on the stock market?")

It’s hard to get excited about Baidu (NASDAQ:BIDU)’s recent performance, with its stock down 9.7% over the past three months. It appears that the market has completely ignored the positive aspects of the company’s fundamentals and decided to focus more on the negative aspects. Long-term fundamentals usually drive market outcomes and are worth paying close attention to. In particular, I would like to pay attention to Baidu’s ROE today.

Return on equity or ROE tests how effectively a company is growing its value and managing investors’ money. In other words, this reveals that the company has been successful in turning shareholder investments into profits.

Check out our latest analysis for Baidu.

How is ROE calculated?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders’ equity

So, based on the above formula, Baidu’s ROE is:

8.2% = CA$22 billion ÷ CA$263 billion (based on trailing twelve months to December 2023).

“Revenue” is the income a company has earned over the past year. One way he conceptualizes this is that for every dollar of shareholders’ equity, the company earned him $0.08 in profit.

What relationship does ROE have with profit growth?

It has already been established that ROE serves as an indicator of how efficiently a company will generate future profits. Now we need to assess how much profit the company reinvests or “retains” for future growth, which gives us an idea about the company’s growth potential. Assuming everything else remains constant, the higher the ROE and profit retention, the higher the company’s growth rate compared to companies that don’t necessarily have these characteristics.

Baidu’s revenue growth and ROE 8.2%

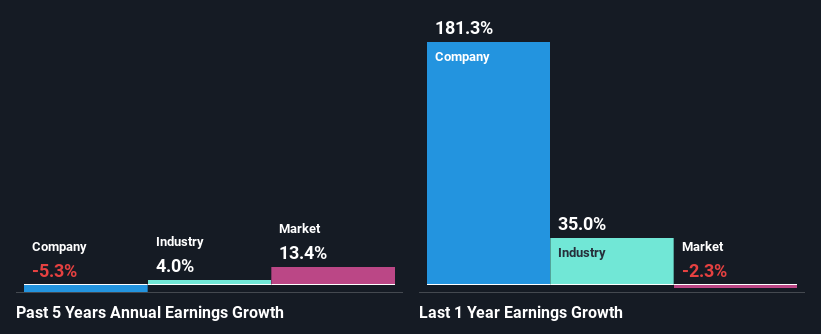

At first glance, Baidu’s ROE does not look very promising. However, given that his ROE for the company is in line with the industry average ROE of 7.9%, it is somewhat of a no-brainer. However, Baidu’s five-year net profit still decreased at a rate of 5.3%. Don’t forget that the company’s ROE is a bit low to begin with. That may be causing the profit growth rate to shrink.

So, as a next step, we compared Baidu’s performance with the industry and were disappointed to find that Baidu has been shrinking its revenues, while the industry has been growing its revenues at a rate of 4.0% over the past few years .

Earnings growth is a big factor in stock valuation. Investors should check whether expected earnings growth or decline has been factored in in any case. By doing so, you can find out if the stock is headed for clear blue waters or if a swamp awaits. Is BIDU fairly valued? This infographic on a company’s intrinsic value contains everything you need to know.

Is Baidu making effective use of its internal reserves?

Baidu doesn’t pay a dividend, so we’d assume all profits are being retained, which is quite disconcerting considering the fact there’s no profit growth. Therefore, there may be other factors at play here that could potentially inhibit growth. For example, businesses are facing some headwinds.

conclusion

Overall, Baidu’s performance is a bit murky. Although the company does have a high profit retention ratio, that low profit margin is probably holding back revenue growth. Having said that, we researched the latest analyst forecasts and found that while the company has seen its earnings shrink in the past, analysts expect its future earnings to grow. Are these analyst forecasts based on broader expectations for the industry, or are they based on the company’s fundamentals? Click here to be taken to our analyst forecasts page for the company .

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.