one year ago you’d have made a 53% return.")

These days, you can easily buy an index fund and (more or less) match the market, but you can significantly boost your returns by picking above-average stocks. Harworth Group The (LON:HWG) share price is 51% higher than it was a year ago, well above the market return of around 6.3% (excluding dividends) over the same period. If this excellent performance can be maintained over the long term, investors would stand to make a killing. However, long-term returns have been less impressive, with the share price rising just 10.0% over the past three years.

It’s also worth looking at the company’s fundamentals here, since it can help determine whether long term shareholder interests are aligned with the performance of the underlying business.

View our latest analysis for Harworth Group

To quote Buffett, “Ships will sail around the world, but the Flat Earth Society will thrive. There will continue to be a wide disconnect between price and value in the marketplace…” One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Last year, Harworth Group grew its earnings per share, moving from a loss to a profit.

When a company is just starting to achieve profitability, earnings per share growth is not necessarily the best way to look at share price performance.

We’re sceptical of the claim that the 0.9% dividend yield will attract buyers to the company’s shares. Unfortunately, Harworth Group’s share price has fallen 57% in twelve months, so a snapshot of the key business metrics doesn’t really paint a clear picture of why the market is buying into the company’s shares at such a high price.

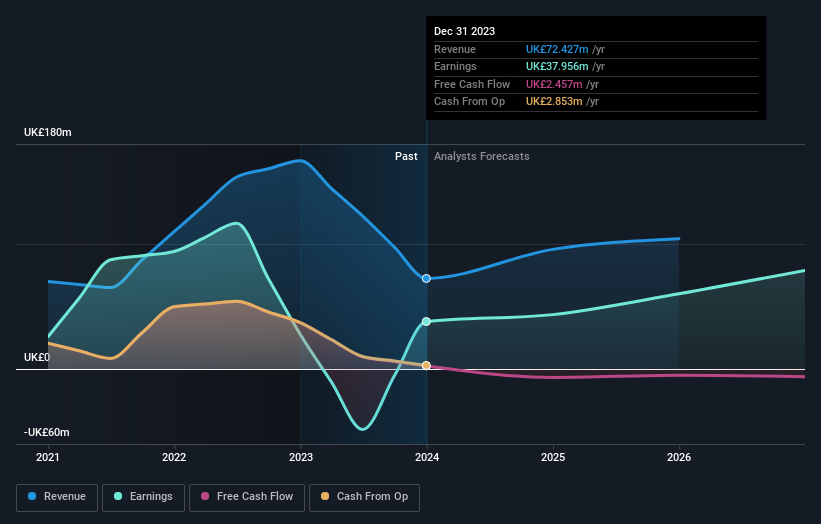

The company’s revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It’s probably worth noting that there has been significant insider buying in the last quarter. While we think this is a positive, we believe revenue and earnings trends are a more meaningful indicator of the business. If you’re thinking of buying or selling Harworth Group shares, you might want to check this information out. free A report showing analyst profit forecasts.

A different perspective

It’s good to see that Harworth Group shareholders have received a total shareholder return of 53% over the past year. This includes dividends, of course. This yield is better than the five-year annualized TSR of 5%. So sentiment towards the company seems to have been positive recently. An optimistic person might view the recent improvement in TSR as an indication that the business itself is improving over time. I find it very interesting to look at share price as a proxy for business performance over the long term. However, to gain real insight, other information needs to be considered as well. For example, we found that: 1 warning sign for Harworth Group Here’s what you need to know before investing.

There are plenty of other companies where insiders are buying up shares, maybe yours too. do not have You don’t want to miss this free A list of undervalued small-cap companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on UK exchanges.

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

Have feedback about this article? Concerns about the content? Contact us directly. Or email us at editorial-team@simplywallst.com