Coalition Greenwich’s analysis of the U.S. credit market found that electronic trading of U.S. credit surged in May 2024. Investment grade (IG) electronic trading reached 49% of total U.S. market volume, its highest percentage on record, while high yield (HY) stagnated at 32%, bringing the total average of electronic U.S. credit trading for the month to 40.5%.

Looking at European credit markets, analysis powered by Propellant’s technology finds that electronic trading across Europe, including both IG and HY, reached a monthly average of 50% in 2024, but fell to 46% in May.

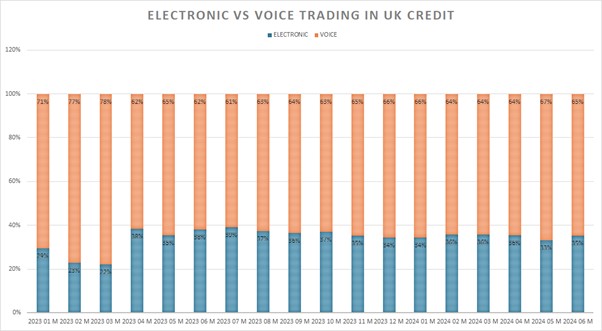

In UK credit trading, monthly electronic trading averaged 35% in 2024, and stood at 35% of total credit trading in May. Propellant’s analysis shows that electronic dealer-to-client (D2C) platforms intermediate activity, while voice is a direct D2C transaction.

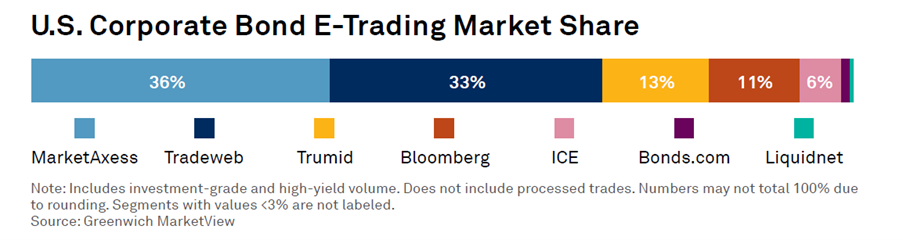

Coalition Greenwich’s analysis of the U.S. market includes a breakdown of margin trading market share among electronic trading platforms, showing that MarketAxess still dominates with 36% of total electronic trading volume, while Tradeweb has grown to 33%. Trumid, which reported its results early, is the third-largest platform with 13%, just ahead of Bloomberg in fourth place with 11%. ICE rounds out the top five with a 6% share.

“We are pleased to see Bloomberg begin reporting U.S. corporate bond trading volumes. [us]”Bloomberg volume reported in MarketView includes TRACE eligible Investment Grade (IG) and High Yield (HY) volume across ALLQ, BOLT, Automated (e.g. Rule Builder) and Portfolio trading services. It does not include TRACE non-eligible trades (trade not involving a FINRA registered broker-dealer), trades booked via VCON or trades via the Terminal’s Single Dealer Page. We believe this view of Bloomberg volume is most closely comparable to other corporate bond exchanges.”

MarketAxess announced that U.S. IG average daily trading volume (ADV) was $6.1 billion, up 6% from market estimated ADV growth of 15%. The strong increase in market volumes included a 35% increase in combined portfolio and inter-dealer trading volumes in May, accounting for approximately 72% of the market’s growth year-over-year, the firms noted.

The firm’s reported U.S. high yield bond ADV was $1.3 billion, down 13%, and its market share fell from 17% to 13%.

“We believe the year-over-year decline in estimated U.S. high yield market share is due in part to lower credit spread volatility and a focus on the new issuance calendar by our long-only client segment,” the firm said in a statement.

Chris Concannon, CEO of MarketAxess, said, “In May, we achieved strong 11% growth in total credit ADV, driven by 22% growth in emerging markets, 25% growth in Eurobonds and 43% growth in muni bonds, with the latter’s market share at a record 8%. Our estimated market share of US high grade portfolio transactions was 22%, up from 13% a year ago and up from 15% in April, reflecting a significant increase in portfolio trading. Approximately 55% of portfolio trading volume was executed on X-Pro in May and we continue to roll it out to our largest clients.”

Tradeweb reported that fully electronic US credit ADV increased 47% year over year to $6.6 billion, while European credit ADV increased 16% year over year to $2.2 billion. The company attributed the volume increase to increased client adoption, particularly of requests for quote (RFQ), portfolio trading and Tradeweb AllTrade, with European credit volume driven by portfolio trading and the company’s dealer selection tool (SNAP IOI) used via automated intelligent execution (AiEX) and RFQs.

In the Treasury space, D2C electronic trading in the U.S. market accounted for 63% of Treasury market activity in May, compared to May 2019, when only 46% of D2C trading was electronic, according to research from Coalition Greenwich.

“The surge in electronic trading makes even more sense when you consider the increase in market-wide volume from 2019 to today,” McPartland noted. “In May 2019, average daily notional volume (ADNV) was $554 billion, of which approximately $255 billion was traded electronically. In May 2024, $823 billion of ADNV will include approximately $520 billion of electronic volume, nearly double. These metrics are another sign of the shift from a market dominated by inter-dealer trading to one where investors are a major driver of trading activity.”

According to analysis by Propellant, electronic trading of UK government bonds accounted for 54% of all D2C trading in the UK and 41% of all D2C trading in Europe in May, while electronic trading of European government bonds accounted for 49% of all D2C trading in the UK and 28% of all D2C trading in Europe in the same month.

Tradeweb’s US Treasury ADV increased 33% year-over-year to $192.5 billion, while European Treasury ADV decreased 0.4% year-over-year to $41.4 billion. The firm noted that US Treasury trading volume was supported by growth across all client sectors, with increased adoption of a broad range of protocols and favorable market conditions contributing to volume growth, as well as a positive impact from the recently acquired r8fin. In Europe, European Treasury trading volumes increased due to market volatility and continued primary bond issuance in Europe and the UK.

MarketAxess announced that total fee ADV in May was US$18.8 billion, up 15% year-over-year.