Shares Have Been Weak Lately, But the Financial Outlook is Positive: Is the Market Wrong?")

It’s easy to ignore Cognizant Technology Solutions (NASDAQ:CTSH), with its share price down 5.2% over the past three months. However, share prices are usually driven by a company’s long term financial health, which in this case is looking pretty strong. In particular, we’ll be looking at Cognizant Technology Solutions’ ROE today.

Return on Equity (ROE) is a measure of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio that measures the rate of return on the capital provided by a company’s shareholders.

Read our latest analysis for Cognizant Technology Solutions

How to Calculate Return on Equity?

Return on equity can be calculated using the following formula:

Return on Equity = Net Income (from continuing operations) / Shareholders’ Equity

So, based on the above formula, the ROE for Cognizant Technology Solutions is:

16% = US$2.1b / US$13b (Based on the trailing 12 months to March 2024).

“Return” refers to a company’s earnings over the past year, meaning that for every $1 of shareholders’ capital, the company generated $0.16 in profit.

What is the relationship between ROE and profit growth?

We’ve already mentioned that ROE serves as an efficient profit-generating indicator to predict a company’s future earnings. We then need to evaluate how much of its profits the company is reinvesting or “retaining” for future growth. This gives us an idea about the company’s growth potential. Assuming all other things are equal, companies with both a higher return on equity and higher retained earnings are usually companies with higher growth rates compared to companies that don’t share the same characteristics.

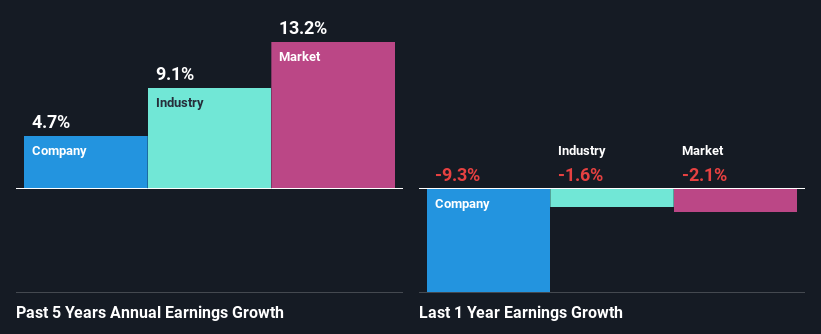

Cognizant Technology Solutions Revenue Growth and 16% ROE

Firstly, Cognizant Technology Solutions’ ROE looks reasonable. Compared to the industry average of 12%, the company’s ROE is quite good. Despite this, Cognizant Technology Solutions’ five-year net income growth rate averaged a very low 4.7%. This is interesting because a high profitability ratio should mean the company has the ability to generate high growth, but for some reason, it has not been able to do so. Possible reasons for this situation include the company’s high dividend payout ratio or the business not allocating capital properly.

Secondly, when compared to the industry’s net income growth, Cognizant Technology Solutions’ reported growth rate is lower than the industry’s growth rate of 9.1% over the past few years, which is not encouraging.

Earnings growth is an important metric to consider when valuing a stock. Investors need to see if the expected earnings growth or decline, in either case, is priced into the price. Doing so will tell them if the stock is heading into brighter waters or if swampy waters await. What is CTSH currently worth? The intrinsic value infographic in our free research report helps visualize whether CTSH is currently undervalued by the market.

Is Cognizant Technology Solutions reinvesting its profits efficiently?

Despite a typical three-year median dividend payout ratio of 26% (or a retention rate of 74% over the past three years), Cognizant Technology Solutions has seen little earnings growth as mentioned above, so there may be other factors at work that could be hindering growth. For example, the business is facing some headwinds.

Moreover, Cognizant Technology Solutions has been paying dividends for seven years, indicating that continuing to pay dividends is far more important to management, even at the expense of business growth. According to our most recent analyst data, the company’s dividend payout ratio over the next three years is expected to be around 25%. Therefore, Cognizant Technology Solutions’ future ROE is predicted to be 16%, which is also roughly the same as its current ROE.

summary

Overall, we feel that Cognizant Technology Solutions has some good things to say. However, it’s disappointing to see that earnings aren’t growing despite the high ROE and high reinvestment rate. We wonder if there are external factors that could be negatively impacting the business. That said, looking at current analyst forecasts, the company’s earnings are expected to gain momentum. For more information on the latest analyst forecasts for the company, check out our visualization of analyst forecasts for the company.

Have feedback about this article? Concerns about the content? contact Please contact us directly. Or email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We use only unbiased methodologies to provide commentary based on historical data and analyst forecasts, and our articles are not intended as financial advice. It is not a recommendation to buy or sell stocks, and does not take into account your objectives, or your financial situation. We seek to provide long-term focused analysis driven by fundamental data. Note that our analysis may not take into account the latest price sensitive company announcements or qualitative material. Simply Wall St has no position in any of the stocks mentioned.

Have feedback about this article? Concerns about the content? Contact us directly. Or email us at editorial-team@simplywallst.com