Most readers would already know that the Symrise (ETR:SY1) share price was up 8.4% over the past three months. Since a company’s long-term fundamentals typically drive market outcomes, we wonder what role, if any, a company’s financials play in price movements. I am thinking. Specifically, we decided to examine Symrise’s ROE in this article.

ROE or return on equity is a useful tool to assess how effectively a company can generate returns on the investment it receives from its shareholders. In other words, ROE shows the return that each dollar of a shareholder’s investment generates.

Check out our latest analysis for Symrise.

How do I calculate return on equity?

of ROE calculation formula teeth:

Return on equity = Net income (from continuing operations) ÷ Shareholders’ equity

So, based on the above formula, Symrise’s ROE is:

9.4% = €345 million ÷ €3.7 billion (based on the trailing twelve months to December 2023).

“Return” is the profit over the past 12 months. One way he conceptualizes this is that for every €1 of shareholders’ equity, the company made his €0.09 in profit.

What is the relationship between ROE and profit growth rate?

So far, we have learned that ROE measures how efficiently a company is generating its profits. Now we need to assess how much profit the company reinvests or “retains” for future growth, which gives us an idea about the company’s growth potential. Generally, other things being equal, companies with high return on equity and profit retention will have higher growth rates than companies without these attributes.

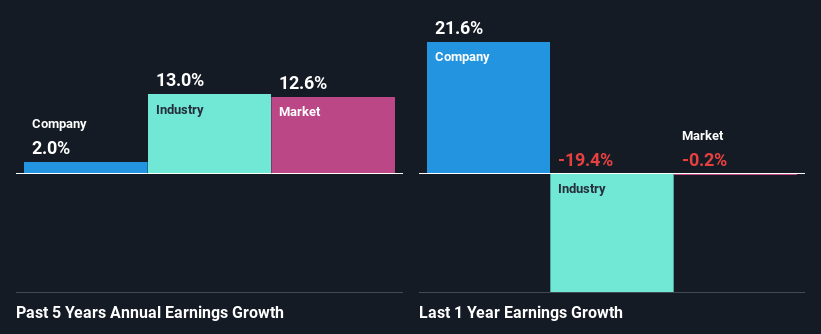

A side-by-side comparison of Symrise’s revenue growth and ROE of 9.4%

First, Symrise seems to have a respectable ROE. Also, when we compare it to its industry, we find that its industry has a similar average ROE of 8.3%. Despite this, his five-year net income growth for Symrise has been completely flat for the past five years. We think there may be other factors at play here that are limiting the company’s growth. For example, the company may have a high payout ratio or the business may have misallocated capital.

We then compared Symrise’s net income growth rate with the industry and found that the company’s growth rate is lower than the industry average growth rate of 13% over the same five-year period, which is a bit concerning.

Earnings growth is a big factor in stock valuation. In any case, investors should seek to determine whether expected earnings growth or decline has been factored in. Doing so will help you determine whether a stock’s future is promising or ominous. What is SY1 worth today? The intrinsic value infographic in our free research report helps you visualize whether SY1 is currently mispriced in the market.

Is Symrise leveraging its profits efficiently?

Symrise’s earnings growth has been roughly It was flat. Therefore, there may be other factors at play here that could potentially inhibit growth. For example, businesses are facing some headwinds.

Additionally, Symrise has been paying dividends for at least 10 years. This means the company’s management is determined to pay a dividend, even if earnings growth means little. Based on our latest analyst data, the company’s future payout ratio over the next three years is expected to be around 35%. However, Symrise’s ROE is expected to rise to his 13%, although no change in payout ratio is expected.

conclusion

Overall, there appear to be some positive aspects to Symrise’s business. However, despite its high ROE and high reinvestment rate, it’s disappointing to see that earnings aren’t growing. We believe there are several external factors that can negatively impact our business. That said, the latest analyst forecasts suggest that the company’s revenue will continue to grow. To know more about the latest analyst forecasts for the company, check out this visualization of analyst forecasts for the company.

Have feedback on this article? Curious about its content? contact Please contact us directly. Alternatively, email our editorial team at Simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary using only unbiased methodologies, based on historical data and analyst forecasts, and articles are not intended to be financial advice. This is not a recommendation to buy or sell any stock, and does not take into account your objectives or financial situation. We aim to provide long-term, focused analysis based on fundamental data. Note that our analysis may not factor in the latest announcements or qualitative material from price-sensitive companies. Simply Wall St has no position in any stocks mentioned.