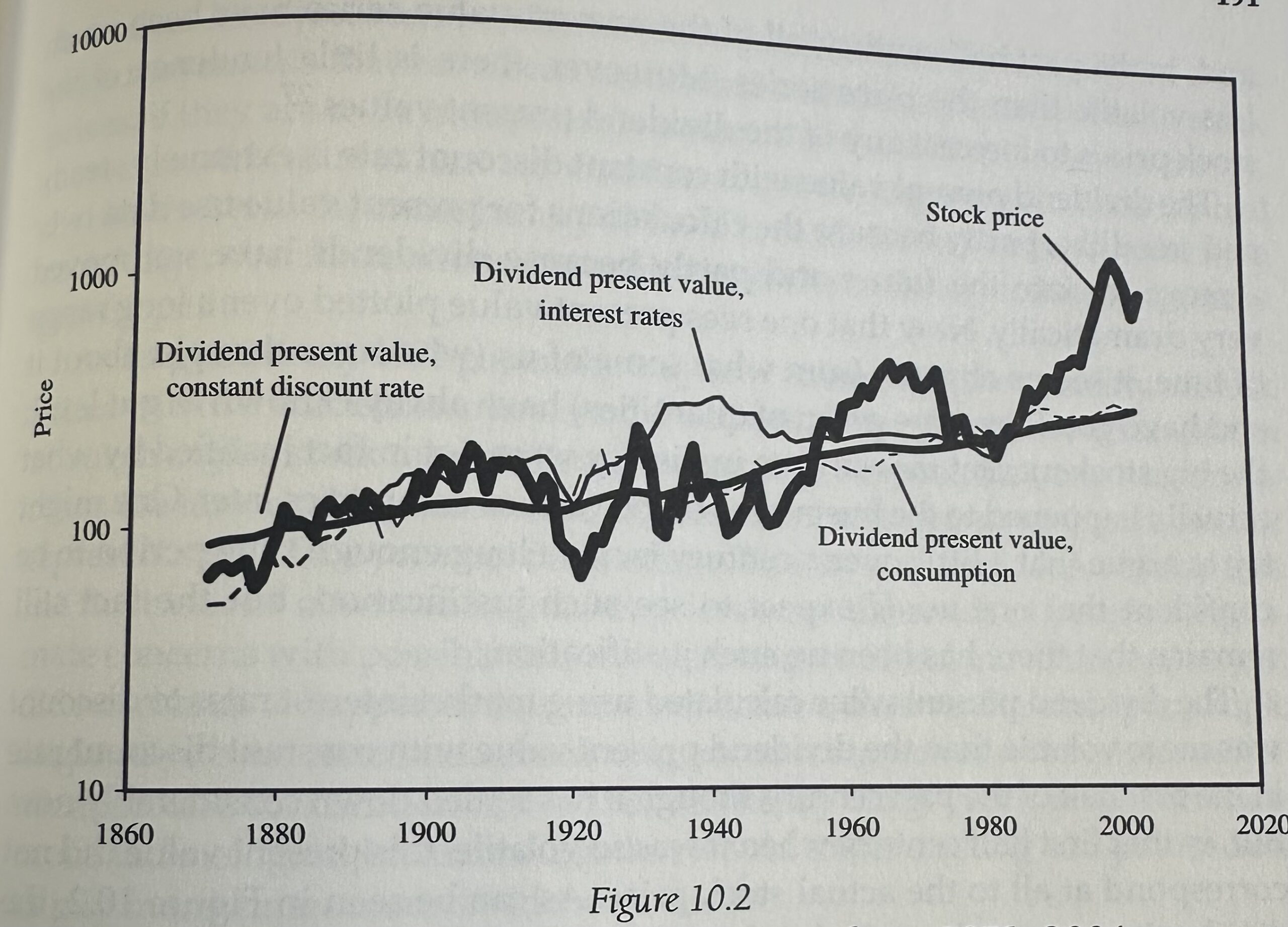

In the early 1980s, Robert Schiller sought to answer the following questions: Will the stock price fluctuate unjustifiably due to subsequent changes in the dividend?

The objective was to understand how well the stock market tracks the present value of future cash flows in the short term.

Shiller concluded: “No, stock prices are not tracking fundamentals very well.”

He updated that data in his book irrational enthusiasm:

Cash flow hardly moves. Prices vary widely.

Shiller points out that between September 1929 and June 1932, the real S&P index fell 81%. The real dividend fell by just 11%. From January 1973 to December 1974, the real S&P index fell by 54%, but real dividends fell by only 6%.

The stock market can sometimes act like a madman, both on the up and down sides.

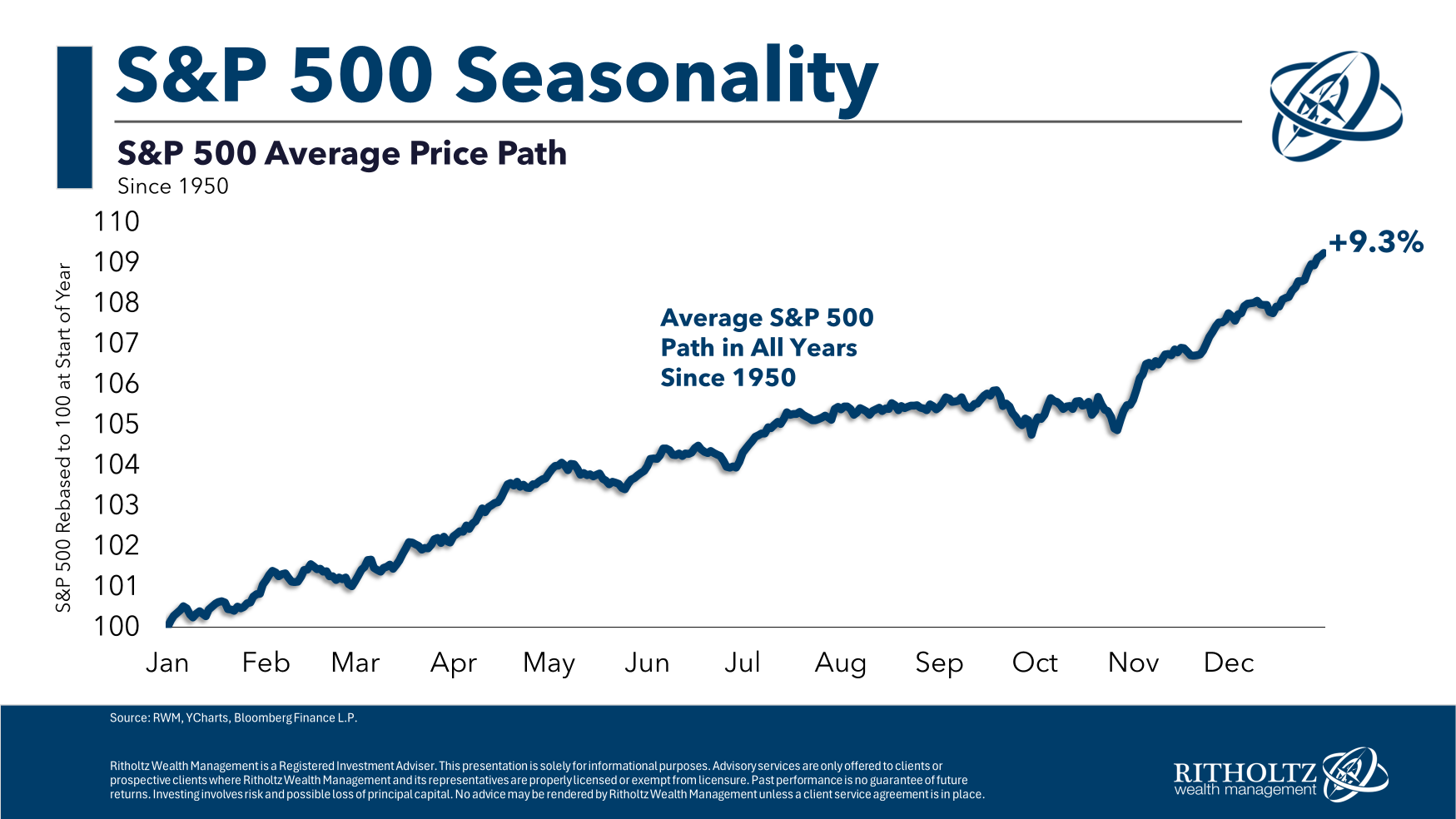

For example, if you take the price performance of the S&P 500 index for each year going back to 1950 and average them, you get:

There are small movements here and there, but overall it’s moving in the right direction: up and to the right.

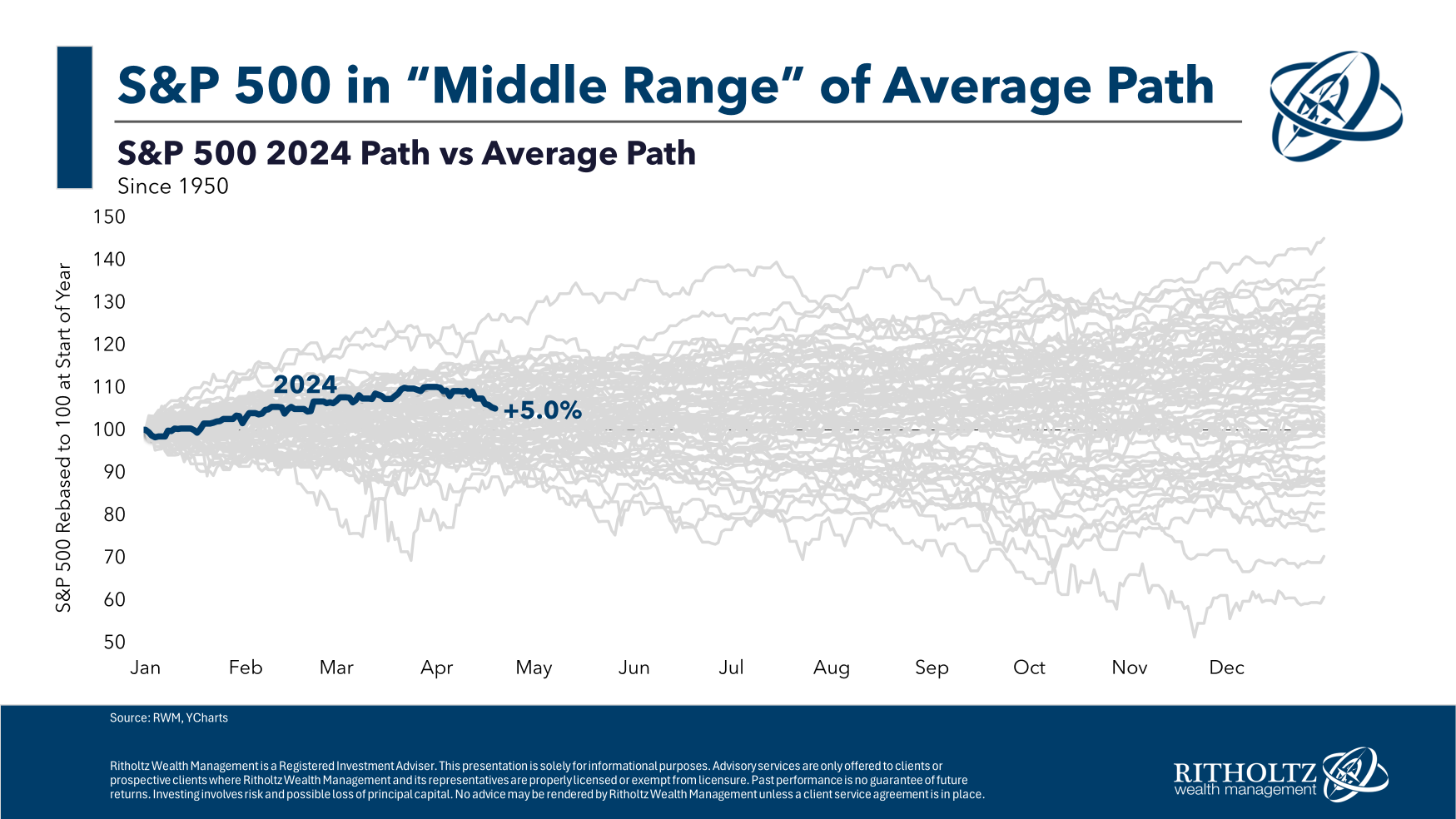

However, when we look at the individual years that make up this average, the range of results varies widely.

There is no such thing as an “average” year in the stock market.

That can’t happen.

If stock market returns were predictable, there would be no risk premium.

Insecurity is a necessary evil.

I was in New York City last week, so I hopped on The Compound and Friends with Josh, Michael, and Art Hogan to discuss things like the “average” number of years in the stock market.

.

References: Pros and cons of investing in the stock market